My first job working in a hotel was in sales at a hotel in Downtown Ottawa in 2014. I will always remember a conversation I was having with a wholesaler and our revenue manager on October 23rd, 2014. It was the day after the attack on Parliament Hill that resulted in the death of Canadian soldier, Nathan Cirillo. The wholesaler, who had traveled in from out of town, asked us how we were doing after the events of the day before. Our revenue manager quickly said “we ended up with 100% occupancy because we were located just outside of the lockdown perimeter”. And I said, “also, we are sad for the loss of life and a bit shaken up.”

The world is not the same place it was 5 years ago. It isn’t the same as it was last year. Climate change and political unrest continue to affect people and businesses all around the world. The ways that people are affected by these changes are difficult to put into words and sometimes beyond comprehension. However, the impact of fires, hurricanes and relocations on the demand for our hotel rooms, can be neatly represented in graphs and charts.

It is important for revenue managers and RMS companies to be aware of these results because they should be taken into consideration when forecasting based on historical data. Using CoStar data, I looked into the impact on occupancy, ADR and revPAR for areas affected by major events in the last years. The events I looked at were spread across North America over the last 10 years, excluding 2020 and 2021.

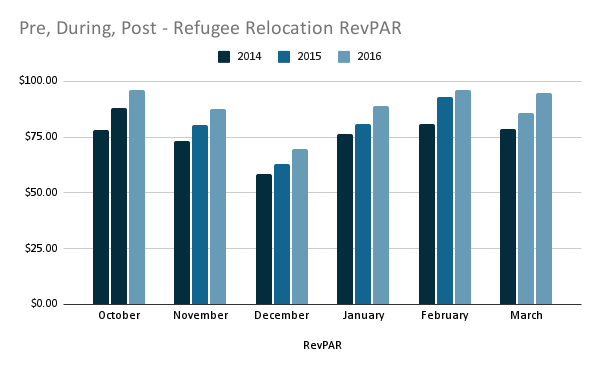

Beginning in 2015, the first event I looked at was the relocation of Syrian refugees in Canada. Over a period of 100 days from November 2015 to February 2016, Canada welcomed 25,000 refugees. Knowing that Toronto was a major hub city for this operation, I looked at the STR data from the Toronto Airport submarket. In order to understand the impact, I looked at the period a year before the events and the following year. So in this case, I am comparing October 2014-March 2015, October 2015-March 2016 and October 2016-March 2017.

The period in question saw ADR growth and Occupancy growth of 4.9% and 4.6% respectively, resulting in revPAR growth of 9.8%. The following year, the submarket saw an increase in revPAR again driven by growth in ADR as occupancy levels remained flat. You can see that February of 2015 saw occupancy levels peak as the deadline of Operation Syrian Refugees loomed.

When preparing for 2016, targets would have been set to accommodate growth over the year before, despite the fact that these numbers were driven by relocations. While occupancy levels didn’t hold for the following year, the ADR was increased as the business came from more varied sources, rather than negotiated rates for longer stays.

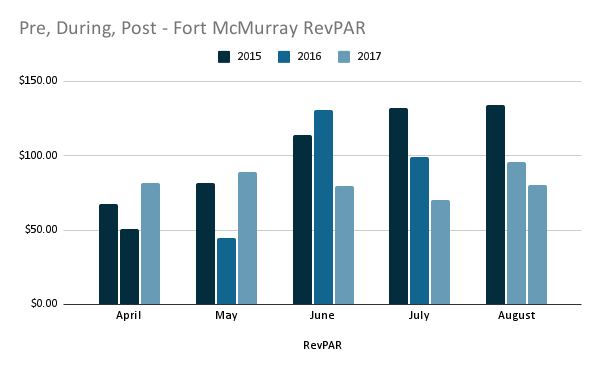

Another Canadian event was evaluated next. The 2016 wildfires in Fort McMurray, Alberta that forced almost 90,000 people out of their homes. The fire began in May and was not declared fully extinguished until August 2, 2016.

What we notice in the revPAR comparison is that typically June through August would see higher demand in Fort McMurray, as denoted by the dark blue columns representing the pre-fire trends. In May 2016 we saw a drop in occupancy to almost 30% as residents were evacuated, and the spike in revPAR in June is driven by residents being able to return to Fort McMurray, but many of them having partially or completely lost their homes.

In 2017 we can see that June and July are not matching up to the 2016 post-disaster numbers, and this is primarily driven by a decrease in ADR. I suspect that the pick-up for room nights was slower than the year before and the rates were reduced as a result (by -22% in June and -13% in July). Occupancy was not lifted by this strategy, and so in August we see revPAR begin to level out with only a 3% decrease in ADR.

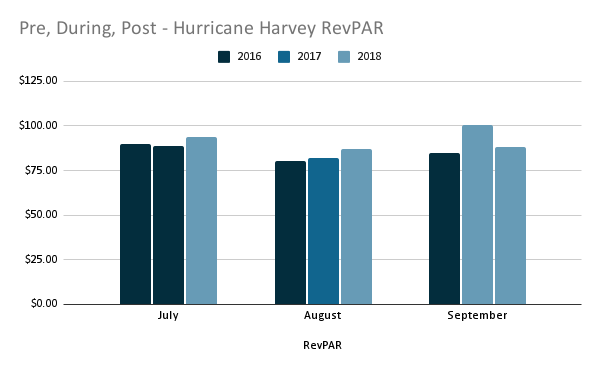

At the end of August 2017, Hurricane Harvey hit Texas causing major flooding and power outages, displacing 30,000 people and destroying 9,000 homes. The hurricane moved on to Louisiana on August 28th, and you can see the revPAR growth in Texas driven by a 14% increase in occupancy in September 2017.

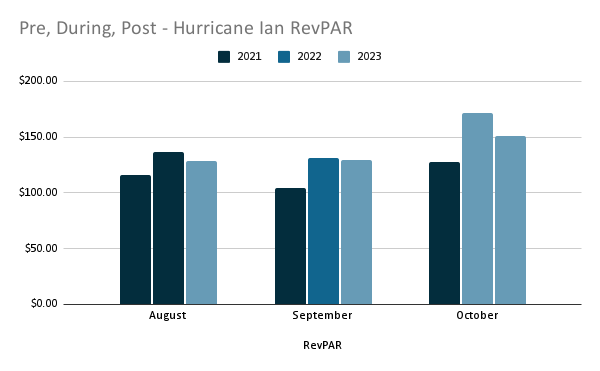

Five years later, Hurricane Ian touched down in Florida. After having caused destruction throughout the Caribbean, the storm was one of the deadliest in Florida’s history with 149 confirmed deaths. From a hotel data standpoint, the state of Florida saw a jump in occupancy rates and ADR in the aftermath as people were displaced due to flooding and destruction.

Based on the year before, we could have expected a dip in ADR of approximately $10 between August and September. Instead we see a drop of only $2. Occupancy also performed slightly better than the year prior with only a 2% drop compared to a 4% drop. It is impossible to say how much of this is due to Hurricane Ian as the storm hit Florida on September 28th and weakened before it continued on to the Carolinas. In October, however, we saw significant growth in RevPAR driven by a 10% bump in Occupancy year-over-year and a $31 increase in ADR.

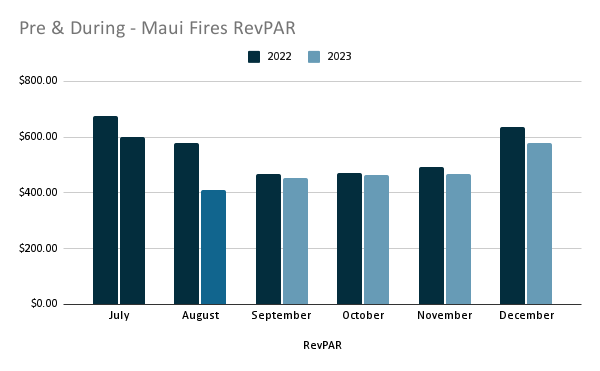

The final disaster I examined happened in 2023 in Maui. The fires there in August 2023, beyond causing billions of dollars of damage and taking lives, also affected the hotel industry. Starting with a drop in occupancy and a small dip in ADR, the months after the events saw higher than usual occupancy levels with rates that were 3%-15% lower than the year before. The impacts continue to be felt through the start of 2024 with revPAR at -6.4% year-over-year in January, -12.4% in February, -11.8% in March and -7.3% in April. Occupancy is seeing some lift as we head into the summer months, but the ADR has yet to return to 2022 levels.

The impact a destination will see from a climate or political event depends on the typical travelers to the destination. While we may be able to anticipate how occupancy and ADR will be affected by certain events, forecasting when and where they will happen is a different ballgame. According to ZestyAI, experts in wildfire risk analytics, fires are no longer “just a California problem”. Concerning drought conditions are seen in New Mexico, Arizona, Idaho and Montana. The government of Canada expects wildfire risk to remain high through the 2024 season in the Canadian West and Atlantic provinces. And the fire seasons have seemingly extended with major fires breaking out earlier than they had in years past.

Now, more than ever, demand forecasting based on historical data is less and less relevant. With various events having caused dramatic shifts in demand over past years, and the possibility of a major climate disaster at any moment, hoteliers need to be ready to think on their feet, react quickly, and capitalize on the good times to ensure they are financially secure to take on the bad times.